Three Steps for Tracking Your Expenses

Editorial Note: Articles published are intended to provide general information and educational content related to personal finance, banking, and credit union services. While we strive to ensure the accuracy and reliability of the information presented, it should not be considered as financial advice and may be revised as needed.

Tracking your spending is the first step toward greater financial awareness and, ultimately, toward financial health. However, mastering this skill is easier said than done. How can you track every dollar you spend when you make multiple purchases each day?

We’ve outlined how to track your spending in 3 easy steps.

1. Choose your tools

Tracing every dollar’s journey isn’t easy, but with the right tools, you can make it quick and simple. Choose from one of the following money-tracking techniques:

- Budgeting apps. If your life happens on your phone, you can download a budgeting app to help you track your spending. Most apps allow you to allocate a specific amount of money for each spending category each month, and will enable you to track your spending with just a few clicks. Just make sure to research apps before downloading them and be aware if the app is free or requires a paid subscription to use.

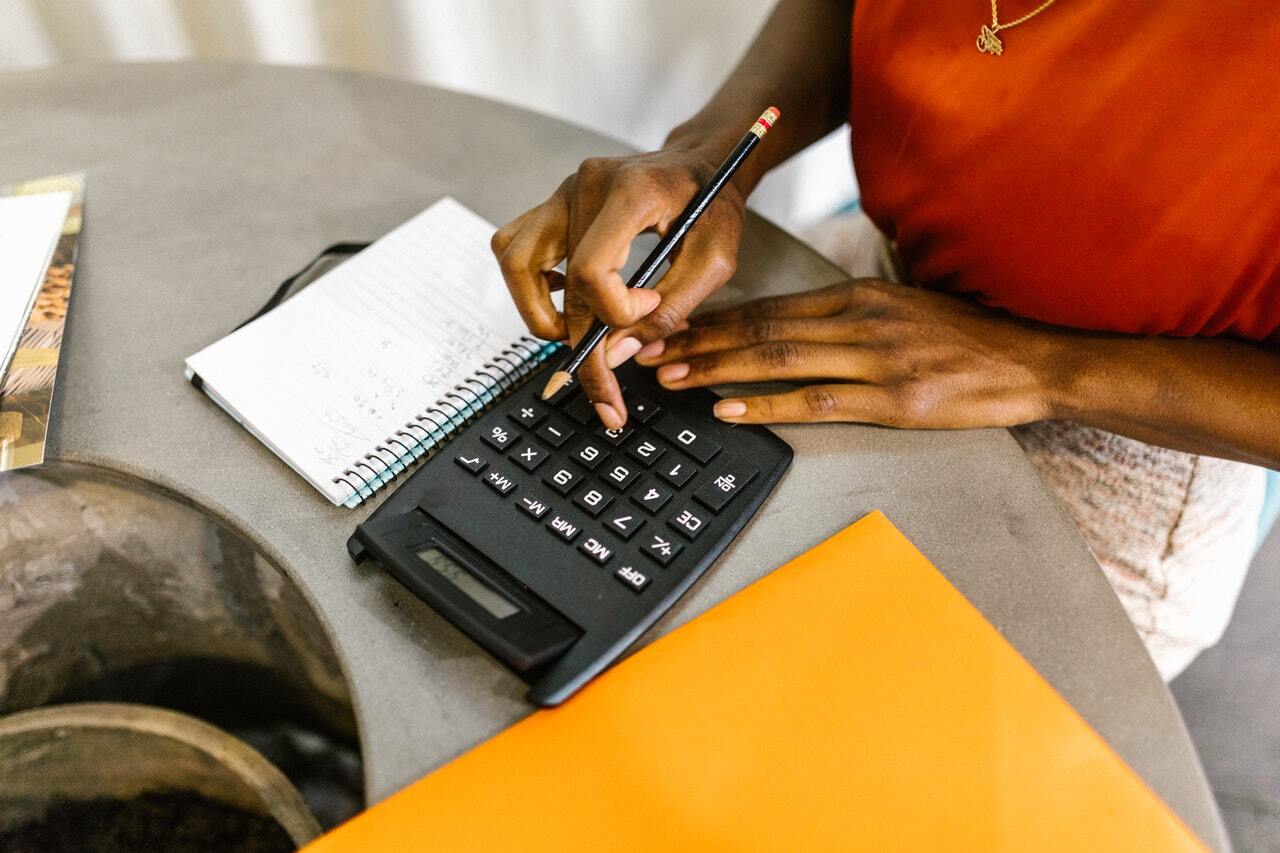

- Spreadsheet. If you like to see everything spelled out clearly, a spreadsheet might be a better choice for you. You’ll need to record every transaction, but if you prepare the sheet with all the spending categories you think you’ll need, this step shouldn’t take long at all. Get started by searching for budget spreadsheet templates online.

- The Envelope System. If you’re a big cash spender, consider withdrawing the cash you think you’ll spend in a month (or in a week) and keep it in an envelope designated for each of your spending categories. When you need to make a purchase, just use money from the envelope. You can learn more about the envelope system here.

- Receipts. Hold onto every receipt from the purchases you make this month to help you track your spending. Folders, pouches or even online software that can help you store and manage your receipts if you prefer tracking this way.

- Pencil and Paper. Recording each purchase the old-fashioned way can help you make more mindful money choices throughout the day. Be sure to keep a steady supply of both writing instruments handy at all times so you never miss a purchase.

2. Review Your Checking Account and Credit Card Statements Carefully

Along with one of the tools listed above, you can track the purchases you make using plastic by reviewing your monthly checking account and credit card statements at the end of the month. You may receive these in the mail, or you can access them online by logging into your account and downloading them.

3. Review and Categorize Your Purchases

At the end of the month, use your chosen tool to review all the purchases you’ve made throughout the month. If you’ve used an app or a spreadsheet, adding your purchases to find the total amount of money you spend is simple. The app or spreadsheet may already have helped you divide the money you spend into separate categories.

Similarly, if you’ve used the envelope system, you should know how much you spent on each kind of purchase this month. However, if you’ve chosen another method to track your spending, you’ll need to crunch some numbers to get an accurate picture of your spending habits.

When completing this step, don’t forget to include automated payments you may rarely think about, such as subscriptions or insurance premiums.

Tracking your spending and identifying where your money might be getting wasted is the first step toward greater financial awareness and responsibility. Use the tips outlined here to successfully master the skill of tracking your spending.

Need additional resources, tools, or even counseling as you navigate your financial wellness journey? Check out Banzai and our range of financial calculators to get started.